Current Affairs

UPSC PRIMARY AGRICULTURAL CREDIT SOCIETIES - English

PRIMARY AGRICULTURAL CREDIT SOCIETIES

Why in news:

- The Union Budget has announced Rs 2,516 crore for computerisation of 63,000 Primary Agricultural Credit Societies (PACS) over the next five years.

- Aim: To bring greater transparency and accountability in their operations and enabling them to diversify their business and undertake more activities.

What are Primary Agricultural Credit Societies?

- PACS are the ground-level cooperative credit institutions that provide short-term, and medium-term agricultural loans to the farmersfor the various agricultural and farming activities. It works at the grassroots gram Panchayat and village level.

- The first Primary agricultural Credit Society (PACS)was formed in the year 1904. Since then, these societies have been playing a significant role in providing short-term and medium-term credit to the farmers. Till the early seventies, this was the only institutional credit agency available to people in rural areas. The PACS functioning at the base of the cooperative banking system constitutes the major retail outlets of short-term and medium-term credit to the rural sector.

Working:

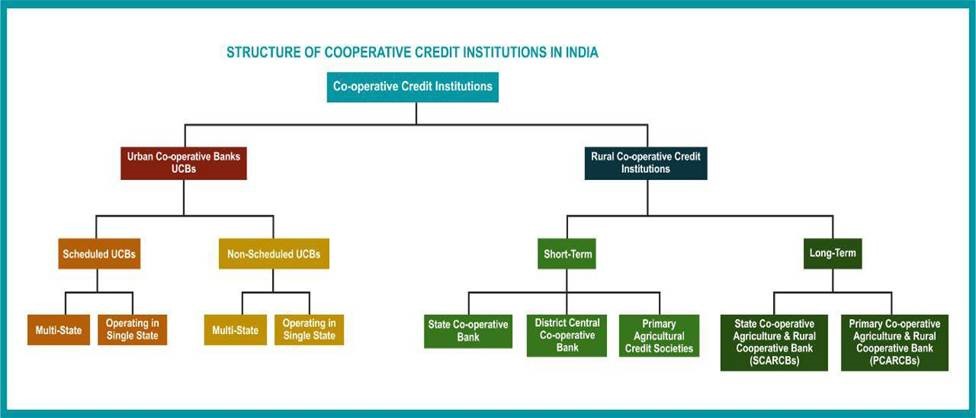

- PACS are village-level cooperative credit societies that serve as the last link in a three-tier cooperative credit structure headed by the State Cooperative Banks (SCB) at the state level.

- Credit from the SCBs is transferred to the district central cooperative banks, or DCCBs, that operate at the district level. The DCCBs work with PACS, which deals directly with farmers.

- Since these are cooperative bodies, individual farmers are members of the PACS, and office-bearers are elected from within them. A village can have multiple PACS

- PACS are involved in short-term lending — or what is known as crop loans. At the start of the cropping cycle, farmers avail credit to finance their requirement of seeds, fertilizers, etc.

Features:

- The Primary Agricultural Credit Societies are the association of persons, unlike in the case of the Joint Stock Companies, where there is just accumulation of capital.

- Primary Agricultural Credit Societies confers equal rights to all its memberswithout considering their holding of share and their social standing.

Organizational Structure

- General Body of PACS: Exercise the control over board as well as management.

- Management Committee: Elected by the general body to perform the work as prescribed by the society’s rules, acts, and by-laws.

- Chairman, Vice-Chairman, and Secretary:Work for the benefit of the members by performing their roles and duties as assigned to them.

Functions of PACS

- To provide short and medium-term purpose loans to its members.

- Borrowing an adequate amount of funds from central financial agencies.

- Maintaining the supply of the hire light machinery for the agricultural purpose.

- Promotes savings habits among its members.

- To make the arrangement of supplying of agricultural inputs. Example -seeds, fertilizers, insecticides, kerosene etc.

- It helps its members by providing marketing facilities that could enhance the sale of their agricultural products in the market at the proper prices.

Significance

- Primary agriculture co-operative credit societies as financial institutions that play a very important role at the grass roots level in the development of local areas. They are multifunctional organizations that dispense a host of activities like banking, on out supplies, marketing produce and trading in consumers goods.

- The Primary Agricultural Cooperative credit societies (PACS) constitute the lowest tier of the three-tier Short-term cooperative credit (STCC) in the country comprising of 13 Cr. farmers as its members, which is crucial for the development of the rural economy. PACS account for 41 % (3.01 Cr. farmers) of the KCC loans given by all entities in the Country and 95 % of these KCC loans (2.95 Cr. farmers) through PACS are to the Small and Marginal farmers.

The major deficiencies of the PACS and their credit are discussed briefly below:

Organizational Weakness

At the primary level, the cooperative credit structure has twofold weaknesses:

(a) Inadequate coverage and

(b) Weak units

Though geographically, active PACS cover about 90% of 5.8 villages, there are parts of the country, especially in the north-east, where this coverage is very low. Further, the rural population covered as members is only 50% of all the rural households.

Why is the borrowing membership low in the PACS?

In the judgement of the Banking Commission, which still holds good, in most cases, one or more of the following reasons are responsible for the low borrowing membership:

(i) Defaults of members in loan repayment and inability of societies to raise resources,

(ii) Inability of the members to provide the prescribed security

(iii) Lack of up-to-date land records or inalienable rights to land or inability to produce sureties,

(iv) Ineligibility of certain purposes for loans.

According to the Banking Commission, in most states, over-dues are due to:

(a) Indifferent management or mismanagement of societies;

(b) Unsound lending policies leading to over financing, or financing unrelated to actual needs, diversion of loans for other purposes;

(c) Vested interests and group politics in societies and willful defaults;

(d) Lack of adequate supervision over the use of loans by the borrowers and poor recovery effort;

(e) Lack of adequate control of banks (CCBs) over the primary societies;

Inadequate and Restricted Credit

Co-operative credit is inadequate in several senses.

First, the PACS provide credit to only a small proportion of the total rural population.

Second, the societies do not provide full credit even for all productive agricultural activities.

The credit given is confined mainly to crop finance (seasonal agricultural operations) and medium-term loans for identifiable purposes such as the digging of wells, installation of pump sets, etc.

Most of the societies do not provide credit for other productive activities undertaken by the agriculturists. Even for approved productive activities, the credit given is usually not adequate to meet in full the need for credit. In most cases, non-agricultural credit needs even for productive purposes are not met at all Consumption loans are generally not given.

Importance of Computerization

- Computerization of PACS, will serve the purpose of financial inclusion.

- It will lead to strengthening service delivery to farmers especially Small & Marginal Farmers (SMFs) will also will become nodal service delivery point for various services and provision of inputs like fertilizers, seeds etc.

- The project will help in improving the outreach of the PACS as outlets for banking activities as well as non-Banking activitiesapart from improving digitalization in rural areas.

- The DCCBs can then enroll themselves as one of the important options for taking up various government schemes(where credit and subsidy is involved) which can be implemented through PACS.

- It will ensure speedy disposal of loans, lower transition cost, faster audit and reduction in imbalances in payments and accountingwith State. Cooperative Banks and District Central Cooperative Banks.

The computerization of PACS has already been taken up by a few states, including Maharashtra.

Way Ahead:

- PACS need to be developed as a One Stop Shopfor meeting all the needs of its member

- PACS have to look for new Business opportunities

- Provide much-needed forward and backward linkages.

- PACS can help transform agriculture into a more financially viable activity

- PACS as Multi Service Centers can help members to become self-reliant and promote rural entrepreneurship- facilitating increased income.

- PACS as Multi Service Centers – can financially strengthen the members, by increasing their income through economic linkages with various sectors of rural economy -Doubling of income (The recent decision by NABARD to develop 35,000 PACS into MSCs in mission-mode is a step in this direction.)

Conclusion

- PACS helps in fulfilling the financial requirements of its members, so their work should not be stopped due to the unavailability of the finances. It makes the loan requirements of farmers and thus helping them in growing their business. The resource-mobilization ‘Capacity of the PACS will improve substantially if, through reorganization and related measures, they are converted into strong and viable units. Then, they should be able to attract both more deposits and more loans from higher financing agencies.

BANK ACHIEVERS Achievers

-

ARUN

BANKING BANKING